How we plan our finances as a couple

A detailed look into our financial planning system - covering budgets, goals, debts, receivables, and how transactions connect everything together.

The beautiful thing about this is how simple our plan is. Our only criterion for it to work is being committed to it, but even more importantly, being committed to one another.

To put it into perspective. We do all our planning on heyFinance. Over the course of the month, I'll probably check my heyFinance account 3-4 times. The first time, on our money date, which takes approximately 1-2 hrs. Then, I'll log in 2-3 times more during the month to double-check if a certain expense was budgeted for, quickly add a new debt/receivable, or just open it to see the beautiful interface and gloss over how organized we are as a couple. This usually takes around 5-15 mins.

To be extra clear, money date refers to the time of the month when we sit together to review our finances—check what happened in the previous month, discuss pending financial issues, if any, and plan for the new month.

Our planning spans 4 categories: Goals, Debts, Receivables, then the Budget that wraps everything together. But I'll also briefly explain how these help us with net worth and how the transactions connect every piece.

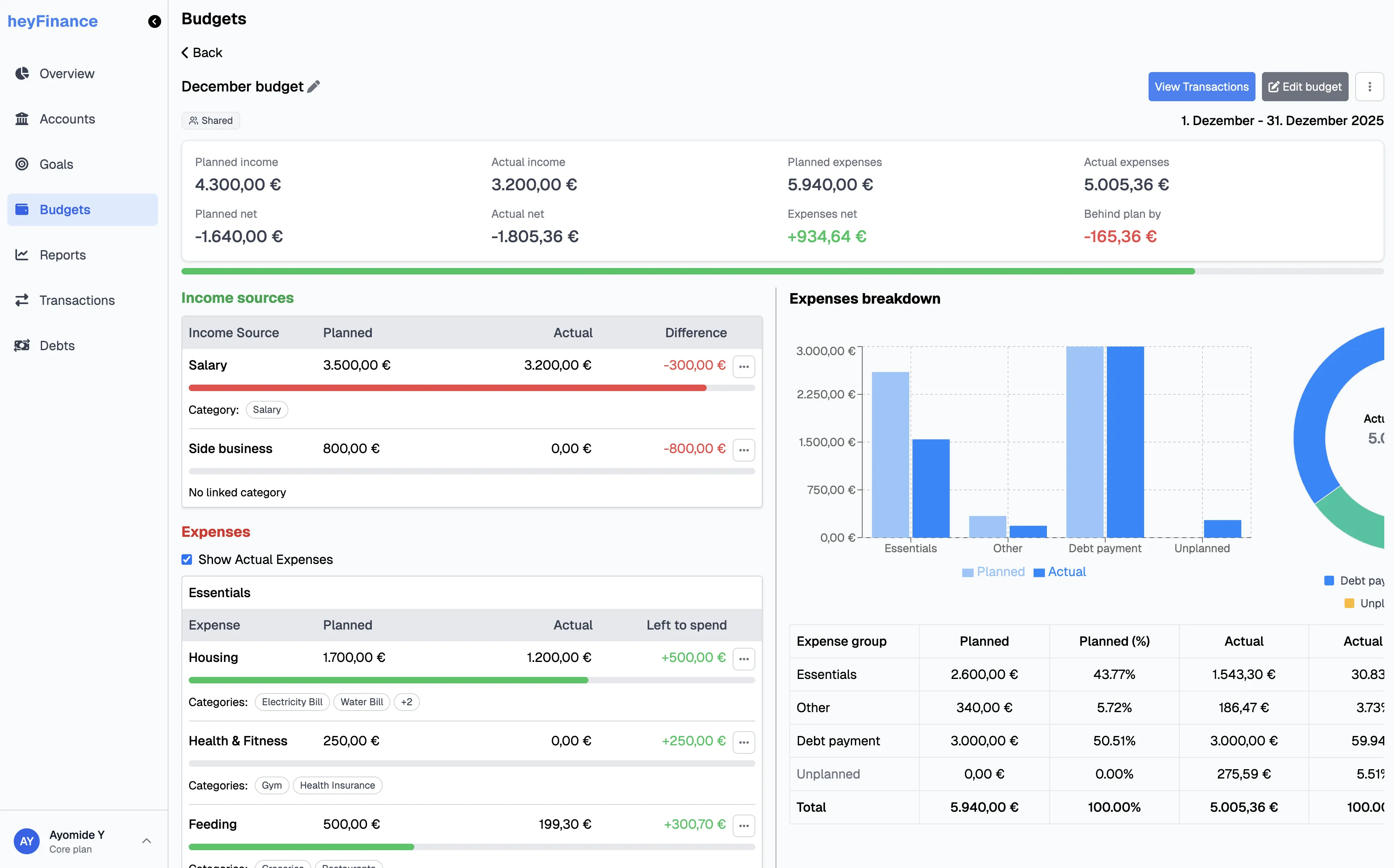

Budget

The budget tells us what we plan to do with money during a certain period. And this is really crucial, because it's like a guide for our finances. A map, telling us, "spend here, not more than this amount, don't spend here", etc.

To be honest, it's really because our money is not yet unlimited, and we have financial goals that we need to plan for. In our budget, or with financial planning generally, we try to plan using a worst-case-scenario approach. We prefer to be positively surprised.

The budget basically answers 3 questions at the time of creation:

- How much are we planning to receive during this period?

- How much are we planning to spend during this period?

- What is the net of 1 and 2? (Planned net) That is, are we adding money to our account? Or taking money from the account to fulfil the budget

After we have our money date, the budget then answers 5 additional questions:

- How much did we actually receive during that period?

- How much did we actually spend during that period?

- What was the net of 1 and 2? (Actual net) That is, did we add money to our account? Or did we take money from our account during the month?

- What was the difference between our planned and actual expenses? (Expenses net)

- What was the overall difference between our planned and actual budget? (Actual net - Planned net)

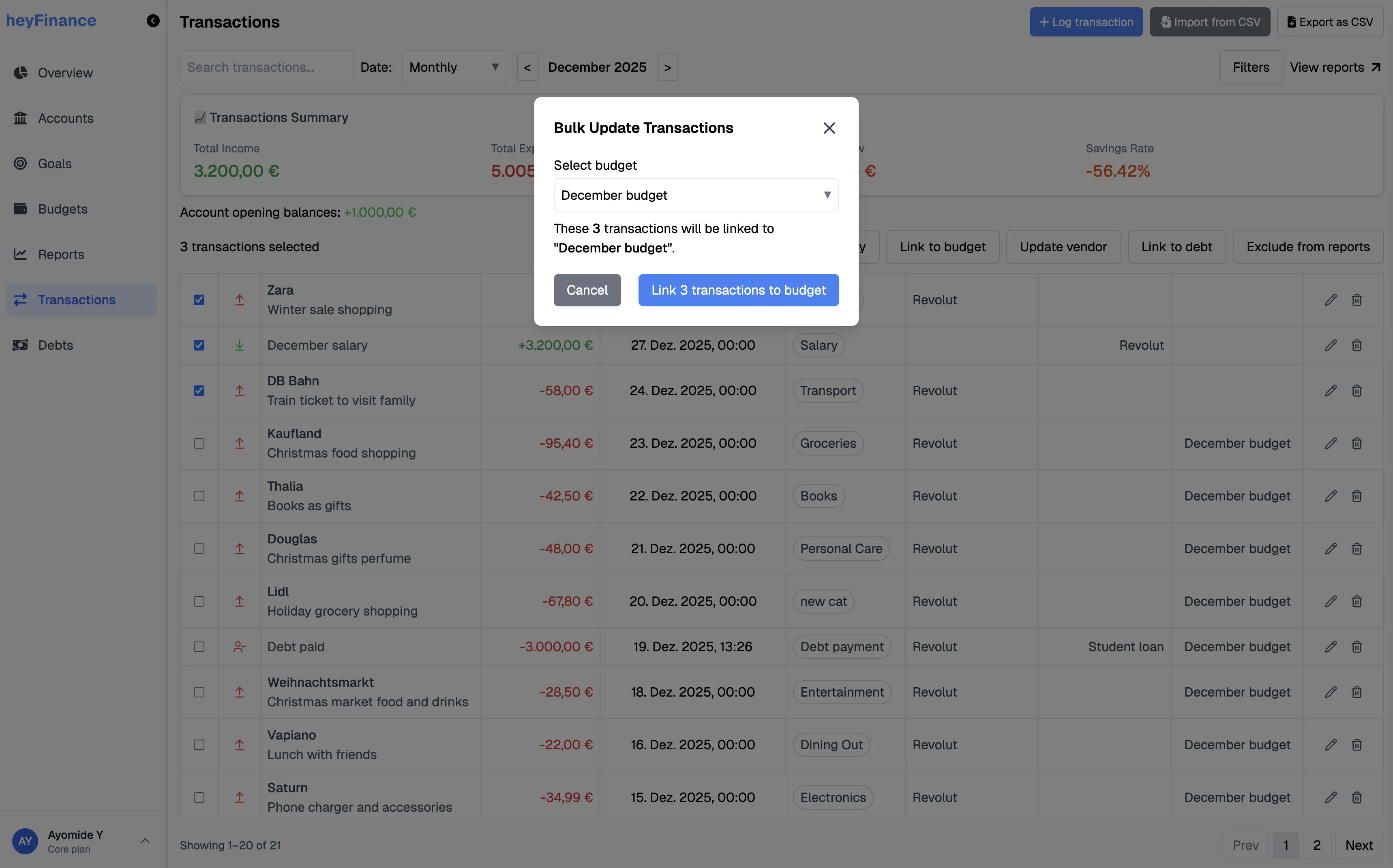

Another very nice thing we do is that our budgets are occasion-specific. We will definitely have 12 budgets for the 12 months of the year, but if we're planning a vacation in July, then we will have 2 budgets in July: one for the month and one for the vacation.

When reviewing the budget at the end of the month, we link the transactions for the monthly budget to the monthly budget, and that of the vacation to it.

More about how transactions link everything together below.

One thing that really helps us here is that after planning, we automate a lot of expenses like rent and investments. We also have group pockets for expenses like Groceries, Miscellaneous, etc and spend from those pockets. This is a very cool feature from one of our banking providers, Revolut.

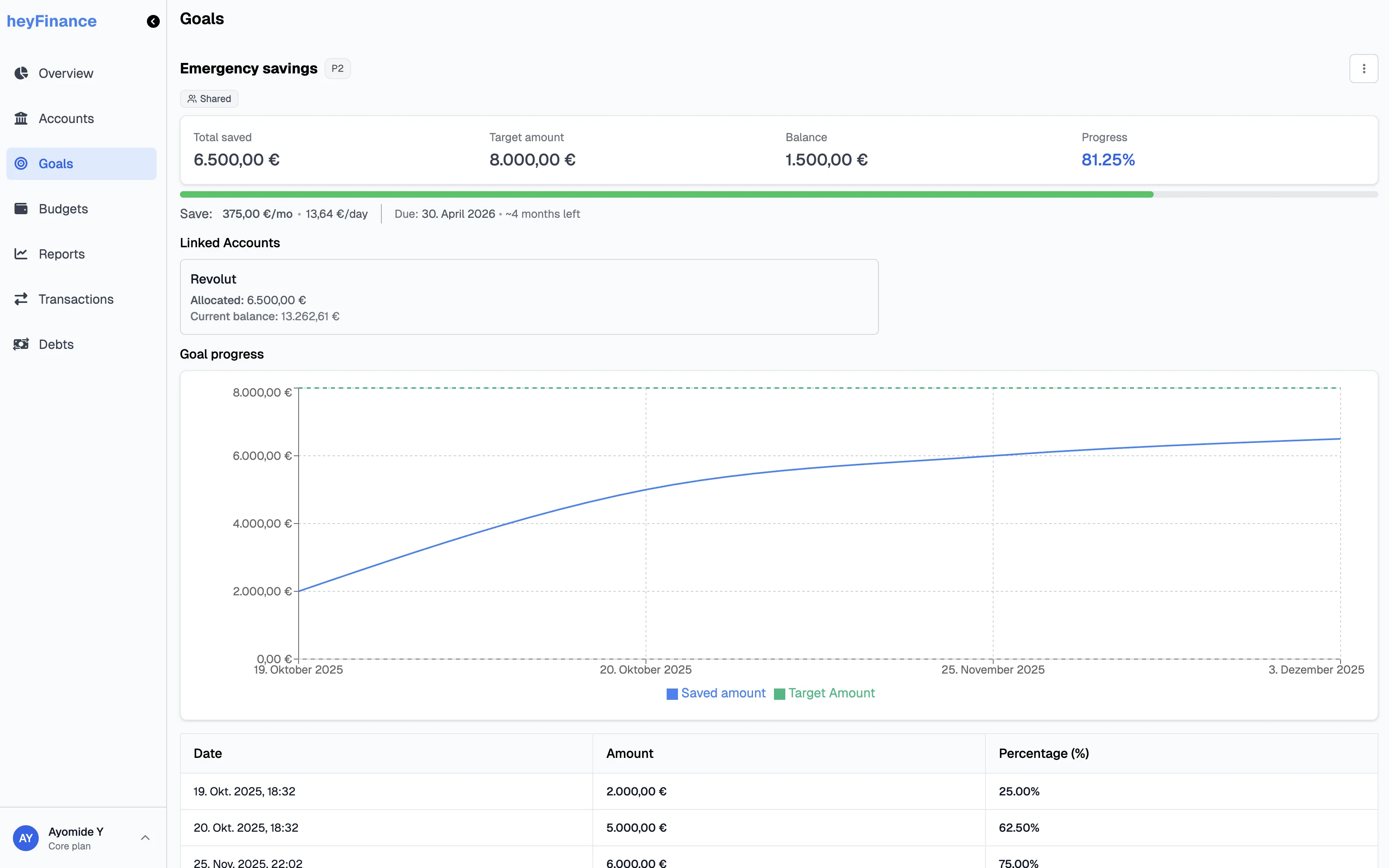

Goals

As I mentioned earlier, the major reason for the budget is that our money is not yet unlimited, and we have financial goals that need to be planned for.

Our goals are the things we look forward to. They are financial milestones we want to achieve. And they can be for security, pleasure, or just out of enthusiasm.

Some of our goals include emergency savings, savings for a mortgage down payment, a car, a vacation, charity, etc.

For us, our goals are allocations of our accounts, which can be exact monetary or percentage allocations. For bigger goals, they are mostly spread across multiple accounts.

Irrespective of the type of goal, we create them on heyFinance, allocate them properly to the right account, see how much we need to save each month, and track the progress over time.

For short-term goals, our Revolut account helps a lot here as we can create pockets or flexible savings accounts and earn up to 3% per annum, which we can withdraw anytime.

For our long-term goals, it's usually split between Revolut savings accounts or invested using Trade Republic or Binance.

We are not affiliated with any of them; we just use them ourselves.

Debts

Debts for us are interesting because they are not just traditional debts—we also create debts for obligations that are not usually part of our monthly budget, or are one-time. For example, if we decide to send a family friend a gift, and we plan to spend €300, we will create a debt for the gift.

Also, when we create a budget for the month, and the planned net is negative, we create a debt for that amount. We delete this particular debt at the end of the budget period.

I'll explain why we do this under Net worth.

Receivables

Receivables are very traditional for us—money that we expect to receive. This can be actual loans to people, to the business, house deposit from our landlord, or some bonus from work.

As I mentioned earlier, we tend to plan finances from a worst-case scenario point of view; so, while we record receivables on heyFinance to track them, there's an option "exclude from net-worth" which we set for most of them. Except the ones we are really sure are coming in.

Otherwise, we assume the money wouldn't come in, and hope to get positively surprised. This is also why we do not create a receivable when we create the budget for the month, and the planned net is positive.

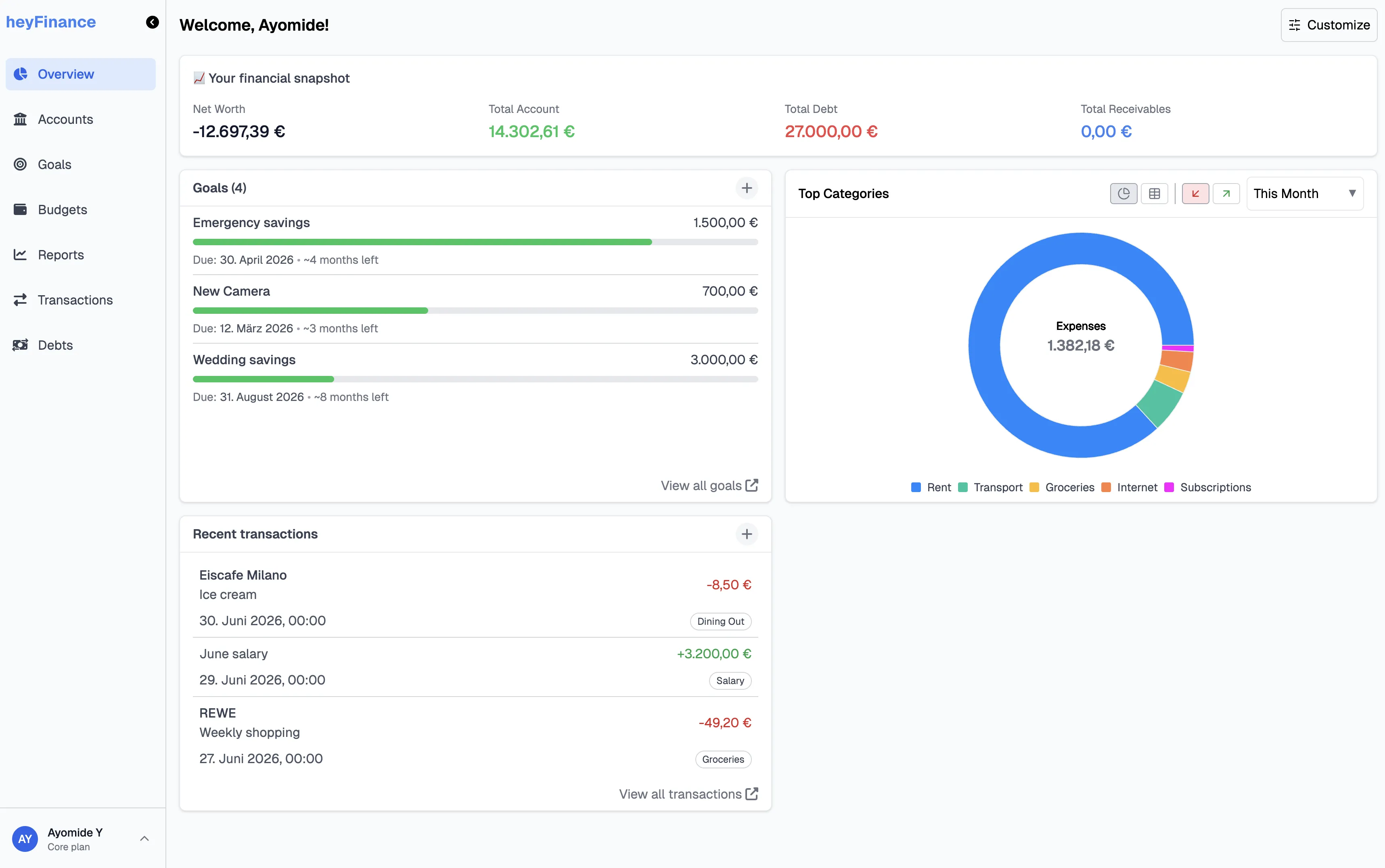

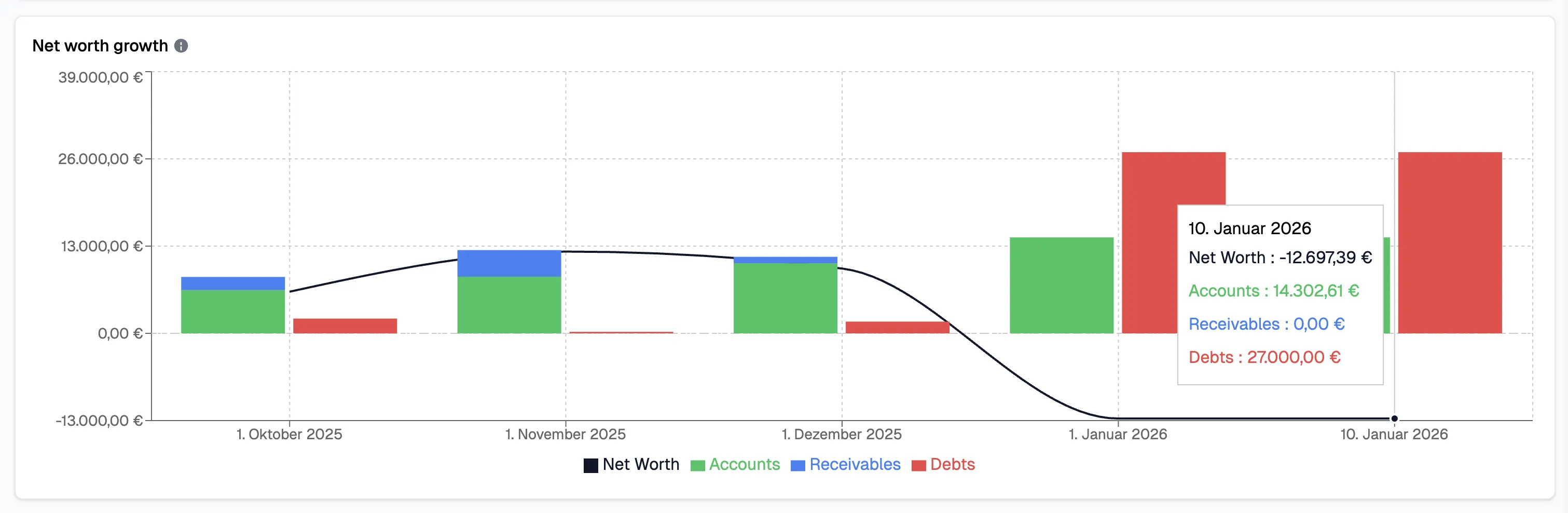

Net worth

Net worth for us is simple: Total accounts - Total debts + Total receivables.

For debts, I mentioned that we create a new entry if we have a budget with a negative planned net. Let's go through this together:

We have our money dates at the beginning of a new month, let's say 4th January, 2026:

- Total account balances - €6,000

- Total debts - €2,400

- Total receivables - €500

Net worth = 6,000 - 2,400 + 500 = €4,100 ✅

Budget for January (let's assume we're finally buying a new couch and dining set):

- Planned income - €2,000

- Planned expenses - €4,500

- Planned net = -€2,500

By creating a new debt with this amount, our net worth becomes 4,100 - 2,500 = €1,600

This basically tells us on the 4th of January that after doing all that's planned for the month, if we pay all debts/obligations and get our receivables in, we would still have €1,600 at the start of February. We'd rather think of things this way than think we have €4,100.

But as I said, we exclude most receivables from net worth, so that will be 1,600 - 500 = €1,100 ✅

This is also why our planning style is so simple. Our budget is set early in the month, our planning is based on worst-case scenario, and we send the money in advance to different pockets from which we spend. Easy!

We love how we can see the net worth overview instantly on heyFinance btw. We can also see the net worth progress over time.

Transactions

This is what really connects all the pieces. Without this, everything is just a plan—the budgets, goals, debts, and receivables.

For our money date, the first thing we do is to get our transactions for the previous month into heyFinance. This is where the magic happens.

We download them from our bank accounts as CSV and import them. For accounts with just a few transactions, we use the bulk-add feature to log them in manually.

Transactions are categorized appropriately, and then linked to budgets, debts or receivables, depending on what happened during the month. This makes it obvious what our planned vs actual looks like. Our net worth also gets automatically updated, and if some money went towards our goals during the month, we update them.

Afterwards, we duplicate the budget, edit a few things for the new month, and that's it.

Side note

One other really cool thing is this: right now, Revolut group pockets have to be created on personal accounts, so they are on my own account. This means my personal account usually has a mix of personal and household expenses.

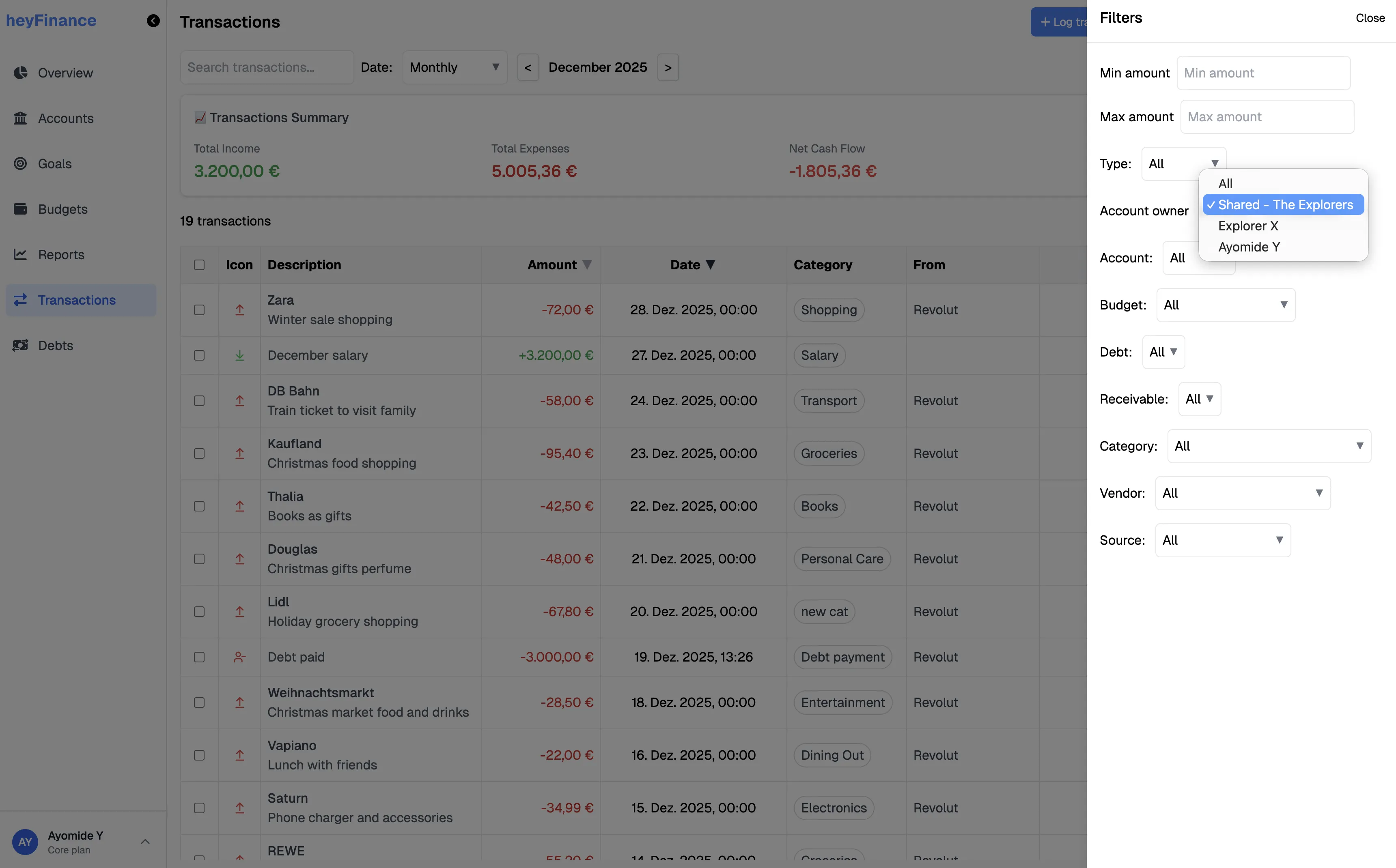

So, on heyFinance, we only link the transactions that are household-related to the shared budget. And this is possible, irrespective of which account the expense was from.

This also means I can easily see how much I spent on personal expenses by filtering by Account owner = Me, Budget = None/A personal budget I had.

This can also be very powerful for couples who want to see how much each partner contributed to the household budget.

And this ownership extends not only to Accounts, but also to Goals, Budgets, Debts, and Receivables. This means I can have a personal budget for a side project I'm working on, in addition to our household budget. Same for personal goals and debts.

In Summary

We use heyFinance for all planning, specifically covering the Accounts, Budgets, Goals, Debts and Receivables. And then, for tracking net worth. We also use Revolut group pockets for expense allocations.

Our planning style is simple. The most important factor that helps us is that we are committed to it, and we're committed to one another.

You think this system would work for you and your partner? Create an account on heyFinance here.

Want to see exactly how we do our monthly money dates? Watch it here

If you liked reading this or found it helpful, you might also like "How we think about money as a couple" to understand our philosophy regarding finances.